Filipinos want a trusted banking partner that offers convenience and innovative solutions for all transactions when it comes to banking. Many international banks out there have established themselves in the country, and CTBC Bank (Philippines) Corp. is one of them.

When it was founded in the 90s, the market for international banks was highly competitive. However, since CTBC Bank entered the scene, it has distinguished itself from its competitors and focused on a niche-based strategy, ensuring they offer innovativeness, efficiency, and a customer-centric approach to individuals and businesses. CTBC Bank ensures that they deliver what it promises through its active partnerships with customers locally.

Written by: Piggyy

Verified by: Krisette C.L

Author

Krisette has been hustling online media industry since 2011. She's a copywriter, editor, and online media consultant.

Piggyy Rating

My Family Home Loan

![]() 4.9/5

4.9/5

Salary Stretch Loans

![]() 4.6/5

4.6/5

Back to Back Loan

![]() 5/5

5/5

SME Business Loan

![]() 4.5/5

4.5/5

Business Loans

![]() 4.3/5

4.3/5

Salary Stretch Loan for Corporate

Get the financing offer that best matches your financial needs and apply for a loan with CTBC Bank.

Bank services

CTBC (Chinatrust Commercial Bank Limited) Bank is an international corporation established in 1966. It’s one of Taiwan’s largest and most well-established, privately-owned financial institutions.

CTBC has service outlets in the U.S., Canada, Japan, India, Indonesia, Hongkong, Singapore, Malaysia, Thailand, Myanmar, Australia, Vietnam, and China. It has expanded its operations in the Philippines through its subsidiary, CTBC Bank (Philippines) Corp.

CTBC Philippines head office is located at 16th to 19th Floors, Fort Legend Towers, 31st Street corner 3rd Avenue, Bonifacio Global City, Taguig City. It is regulated by the Bangko Sentral ng Pilipinas and is compliant with Philippine laws.

Customers can reach out for any concerns and inquiries to the customer service during banking hours from 9:00 AM to 4:00 PM. Other contact details include:

Tel (Manila): +63 (2) 8840 1234

Toll-Free (Other Provinces): 1 800 10 840 1234

International Toll-Free: IAC + 63 + 2 + 840 1234

Email: [email protected]

Email inquiries should include your full name, company name, landline, mobile number, and the Product(s) and/or Service(s) you’re interested in.

Buying a new home or property for your growing family can be delayed due to financial constraints. However, CTBC Bank provides a straightforward, hassle-free process for housing loan applications.

Loan Amount: ₱500,000 up to ₱50,000,000

Loan Term: up to 20 years

Interest: prevailing home loan rate at the time of availing

Loan Processing Time: 5 banking days

Salaried Individuals, Professionals or Self-Employed who:

For Salaried Individuals:

For Professionals and Self-Employed:

This is an unsecured loan for salaried individuals, salaried individuals in the call center industry, self-employed individuals, employed doctors, self-employed doctors or consultants that can be availed for a short-term or mid-term purpose. The repayments for this loan are through post-dated checks (PDCs).

| Eligibility | Requirements |

|

Original copies of the requirements may be required prior to loan release. Other documents may also be required by the Bank. |

| Eligibility | Requirements |

|

|

| Eligibility | Requirements |

|

|

| Eligibility | Requirements |

|

|

A type of multi-purpose unsecured personal loan to employees of accredited companies where employees can avail of competitive loan amounts and flexible terms. Loan repayments are done via a salary deduction.

Company Pre-Accreditation

| Company Post Accreditation

|

Existing depositors on savings and time deposits may sometimes face financial gaps in their businesses or personal finances. If they need extra funds for personal use or expansion of business, they can borrow against their account through this type of loan.

Loan Amount: minimum of ₱100,000 and borrowed against the account holder’s Savings or Time Deposit account.

SME Business Loan is available to small and medium-sized enterprises looking at secured financing to address their business needs. Currently, CTBC offers two types of SME Business loans: Short-Term Loan or Revolving Credit Line and a Term Loan.

For SMEs whose main concerns are the short-term funds needed for the company to operate on a daily basis or for working capital requirements, this is the type of loan that SMEs should go ahead with.

When a SME’s business goal requires long-term financing, the loan term is the most ideal option for them. They can pay the loan in monthly amortizations for a term that could go up to 10 years.

Loan Amount: ₱500,000 to ₱70,000,000

Loan Term:

Processing Time: 21 banking days

Interest rate: Prevailing SME business loan at the time of availing

Interest rate fixing:

Collateral: Real estate properties

| Eligibility | Requirements |

| Proprietorships, Partnership and Corporations who:

|

|

There are different types of products under Business Loans:

It is established to facilitate short-term business operations and cover the expenses during normal business operations before a company realizes cash.

Long-term financing that company engages in for plant expansion and purchasing non-current assets for the company’s long-term operations.

This type of financing is composed of two or more banks or investors to facilitate large-scale loan borrowings where each bank or investor participates as a lender in the facility.

A multi-purpose credit line may be drawn on a one-time or multiple basis.

A type of credit line granted by the bank against an assignment of post-dated checks issued by the bank-customer’s vendors. Repayment of the loan is taken from the proceeds of the matured post dated checks.

A type of financing product where the bank purchases current dated checks.

CTBC Bank has proven its excellent service over the years by establishing over 152 branches in Taiwan and 260 branches worldwide. With its dedication to promoting sustainable sources of financing, it conducts various banking practices such as lending, borrowing, investing, and even cash management that help customers become financially stable.

CTBC Bank’s commitment to providing outstanding service has gained the trust and confidence of its customers aside from its numerous achievements and awards in the Philippines and overseas.

CTBC Bank (Philippines) Corp. is regulated by the Bangko Sentral ng Pilipinas (BSP) and a member of the Philippine Deposit Insurance Commission (PDIC) and BancNet.

CTBC Bank offers a wide array of financing products that enable clients to get all the financing they require, whether for operating capital increase, day-to-day business expenses, or growth.

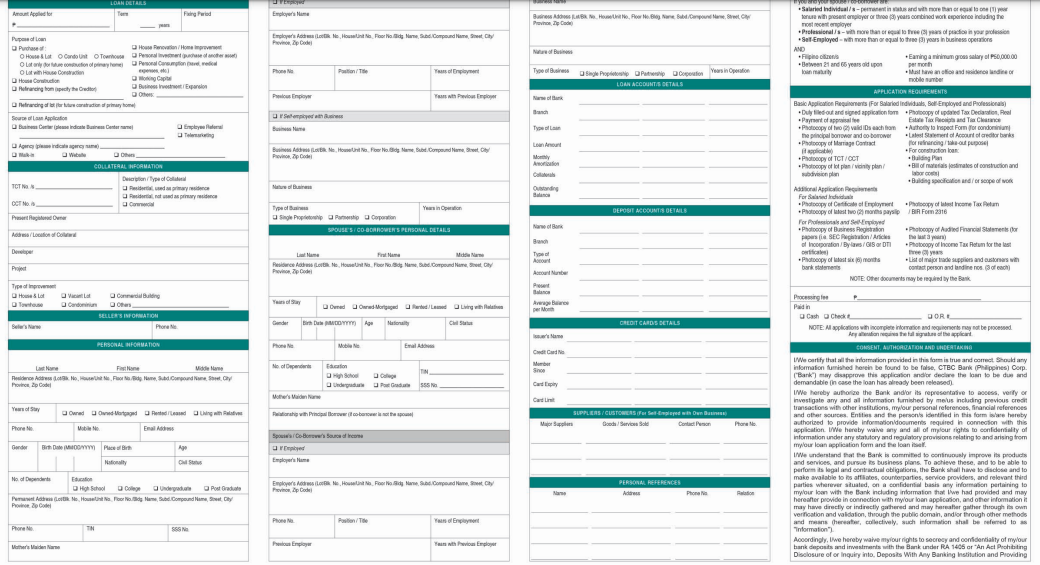

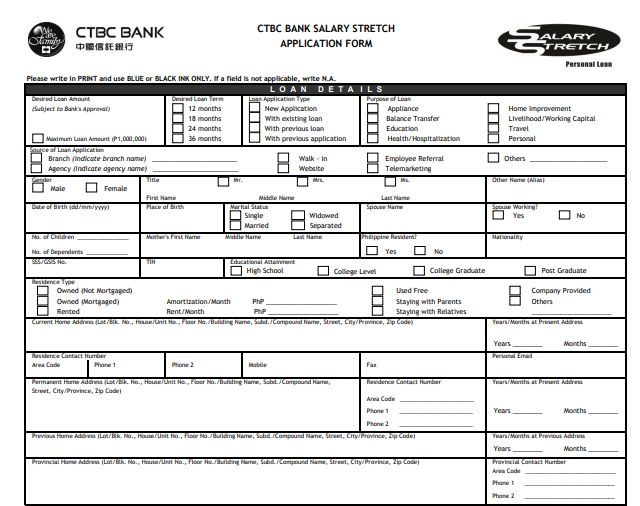

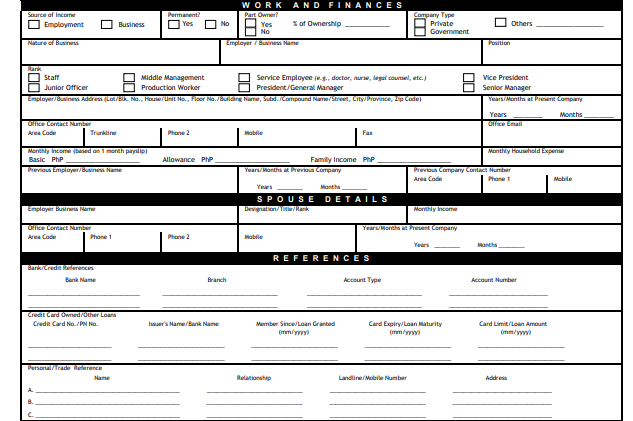

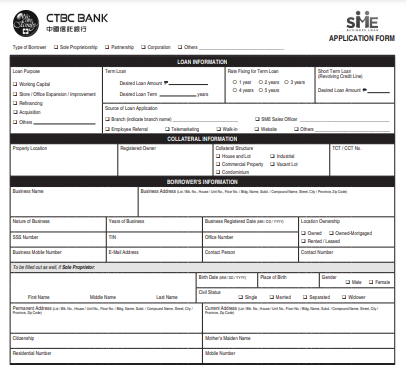

To apply for a loan with CBTC, borrowers may download the application form online through their website.

Loan application forms will look like this:

Home Loan:

Salary Stretch Loan:

SME Business Loan

Once the application form is filled, customers can also prepare the complete requirements to be submitted along with the application form to any of the CTBC branches near them.

Different types of loan borrowing are suited for your financial needs. CTBC Bank is a reputable financial institution that offers great deals and the best customer service.

It has carried out its promise to achieve sustainable growth and to be a trustworthy brand that provides a uniquely personal and fulfilling customer experience through differentiated products and services. Filipinos looking at the best offers for financing cannot go wrong with CTBC Bank.

״The secret of happiness, is not found in seeking more, but in developing the capacity to enjoy less״ - Socrates

Table of Contents

Share this article:

״The secret of happiness, is not found in seeking more, but in developing the capacity to enjoy less״ - Socrates

Table of Contents

Share this article:

״The secret of happiness, is not found in seeking more, but in developing the capacity to enjoy less״ - Socrates