Quick Info on Loans Canada:

- Main Office: 1801-1 Yonge Street, Toronto, ON, M5E 1W7

- Business Hours: Mon – Fri: 9:00 AM TO 5:00 PM (EST)

- Email: [email protected]

- Phone: 1(877) 995-6269

Types of loans offered

Personal Loans

These are loans intended to cover significant expenses such as weddings, urgent travel, or other emergencies. Securing a personal loan does not require an asset to guarantee the loan. However, the lender will assess the borrower’s credit score to determine creditworthiness and the rate of interest to charge. Loans Canada partners offer $50,000 as the maximum personal unsecured loan.

Debt Consolidation Loans

This program aims at setting up a system for the management of a person’s debts. All high-interest debts merge into a single loan with low interest through the consolidation program. The reduced interest payment makes it easier to settle the entire debt through affordable monthly payments. The type of debts that may be consolidated include;

- Credit card debt

- Unsecured personal loan debt

- Auto repossession debt

- Non-government student loan debt

- Past-due cell phone

- Medical bill debt.

Car Loans

These are loans drawn out to buy vehicles. The borrower is usually required to surrender his car as collateral. Such a borrower may have his vehicle seized or sold if he defaults in paying back the loan borrowed. Loans Canada partner lenders provide financing for new and used cars, refinancing, and financing vehicle repairs. Depending on the lender, repayments (plus interest) for car loans can be made weekly, bi-weekly or monthly.

Car loans for used cars do have specific limits set up by lenders. For example, lenders do not grant loans for used vehicles where the amount involved is far higher than the car’s value in question. This is because cars are subject to depreciation, and in the case of default in repayment, the lender may not regain the amount loaned out even after the sale.

Costs Involved in Auto Financing

Interest: The interest paid on car loans varies from lender to lender. It is advisable to consider the rate of interest involved before contracting with a lender.

Loan Term: Both long and short loan terms have their advantages and disadvantages related to monthly repayments and interest.

Short-term loans = high monthly payments + less interest.

Long-term loans = less monthly payments + high interest.

Fees: Fees paid on car loans may include administrative fees, origination fees, penalty fees which only arise in case of breach of agreed terms.

Types of Car Loans and Loan Terms

The following are types of car loans offered by loans Canada money-lending partners;

Auto Refinancing involves drawing out a new loan to settle the original loan expended to purchase the car. Afterward, installments would be made to pay the latest loan plus interest.

Term: 2 to 7 years

Rent-to-own: In a rent-to-own car loan program, the borrower makes several installment payments over an agreed period. On the contracted date between the parties, the borrower will then have the option to purchase or return. If the borrower chooses to buy, the initial payments made will operate to cover a part of the cost price of the car.

Term: 1-2 years

In-House Financing: The dealer pays for the borrower’s desired car. Such an amount will later be repaid in installments plus interest over an agreed period.

Term: up to 5 years

Lease to buy: This involves making steady payments over an agreed period. At the end of the agreed period, the borrower may take out a bank loan to effect a purchase or secure the purchase price from a third-party money lender.

Term: 3-5 years

Documents Required to Secure a Car Loan

To avoid being rejected by a to-be lender, make sure the following documents are intact:

- Valid driver’s license

- Car insurance

- Proof of income

- Photo identification

- Valid address

- Active bank account

Small Business Loans

Loans Canada services also include matching Canadians with lending partners willing to provide loan funds for businesses. Business loans are usually unsecured up to $300,000 with no required collateral. There is no standard limit to how much you can borrow for your business. However, the loan amount will depend on how much the lender thinks it safe to release, the amount needed, and creditworthiness.

Types of Business Loans

Commercial Mortgages

This type of loan is taken out to purchase a commercial property, business upgrade purposes, or expansion. The property purchased with the loan automatically becomes the collateral for the obtained loan.

Commercial mortgage loans can range from 5 to 30 years, depending on the lender. Lending firms usually contract to finance a portion of the property value, which may be within the range of 65% to 75%.

Business Line of Credit

A business line of credit may be secured or unsecured. It operates like a cash advance with low interest and higher credit limits. The line of credit may be accessed anytime as long as the borrower makes payments on time and does not exceed the credit limit.

A business line of credit is perfect for meeting the daily needs of a business operation. The available loan amount depends on whether the line of credit is secured or unsecured and other requirements set by the lender to determine the loan amount.

Equipment Financing

Equipment financing loans are expended to purchase the borrower’s business operation equipment. Usually, the purchased equipment becomes the collateral and will be seized in case of default.

Typically, the amount disbursed as the loan will be repaid plus interests in installments over an agreed period. However, some lenders may refuse to finance the entire purchase price or suggest a different type of equipment.

Inventory Financing

This is a secured loan in the form of a line of credit meant to purchase inventories from suppliers. The purchased items, being collateral for the loan, will be seized in case of default. Inventory financing is perfect for business owners struggling to pay suppliers or trying to restock. The available loan amount depends on how much the lender is willing to release and the borrower’s creditworthiness.

Credit-Building Loans

Having bad credit makes lenders and other financial stakeholders a bit suspicious of getting into business with you. A good way of raising your credit score is to take out a loan and repay it religiously.

Since traditional banks will not even consider granting a loan to someone with bad credit, you can apply for a credit-building loan. This loan operates differently from conventional loans since there is no emergency or need. The loan amount granted is kept in an account until repayments are complete. After which, the principal will be released to you. Although, a loss may be incurred in respect of interest paid during the course of the loan.

The lender will report the payments to Canada’s two main credit bureaus. Also, the transaction will reflect on your credit report and boost your credit score.

Loans Canada services include connecting Canadians with lenders who can help them build their credit scores.

Home Equity Loans

Homeowners can take out a home equity loan to borrow against the value of their home equity. Home equity value is the difference between the home value and the mortgage balance. Most lenders give out loans up to 85% of their home equity.

Although home equity loans have low-interest rates, the downside is that the home serves as collateral, and the lender may seize the property in case of default. Loans Canada services link you up with lenders who provide home equity loans.

Features of Loanscanada services

Research: This is probably the primary feature of loans Canada services. Most people do not have the patience or time to conduct in-depth research on all the banks and lenders that offer loans. This may result in taking a loan from a lender that does not match the borrower’s needs.

All that Loans Canada requires is that you supply information in their application form, and they will connect you to the most suitable lender in Canada. Due to Loans Canada accumulated knowledge of lenders, your chances of rejection even become very slim.

Borrower’s Community: Loanscanada mode of operation allows borrowers to rate and review the linked lenders. This will enable you to judge if the lender recommended is right for you. The review system also serves as a form of accountability to lenders.

Long-term financial stability

In addition to their services, Loans Canada also sees your overall financial growth. They make arrangements to assist customers in settling their debt to raise their creditworthiness. Through their learning center, they help customers to sound financial decisions that guarantee financial growth.

Benefits of Loanscanada Services

- Loans Canada tends to have a researched list of suitable lenders for you.

- The application process is simple and only requires you to supply basic information about yourself and your financial status.

- After being provided with the best possible lenders, it shortens the time of approval, making funds accessible to you as soon as possible.

- Loans Canada services are accessible to borrowers, but they receive a commission from the lender you secure the loan from.

- With Loans Canada, you may obtain loans up to $50,000.

- You may secure a loan even with bad credit.

- Data and information supplied to loanscanada are secure, and your connection is encrypted.

Am I Eligible for Loanscanada Services?

Eligibility is based on your creditworthiness. Though a high credit score is not required, a very low score may turn away most lenders. On average, you will have at least two lenders who will be willing to approve your application.

Overall, loanscanada is best for people who need cash within 48 hours, with light credit history and low credit scores. This may include immigrants and people on the verge of bankruptcy

How to Apply for Loanscanada Services

Start by clicking below:

Then, click “apply now” in a green box on the landing page.

Select the category of loan you are applying for from the available options.

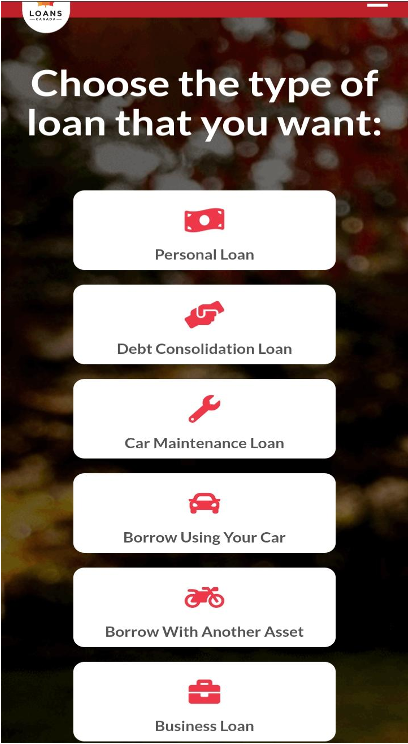

The next page will require you to choose the specific loan you are applying for from the available options.

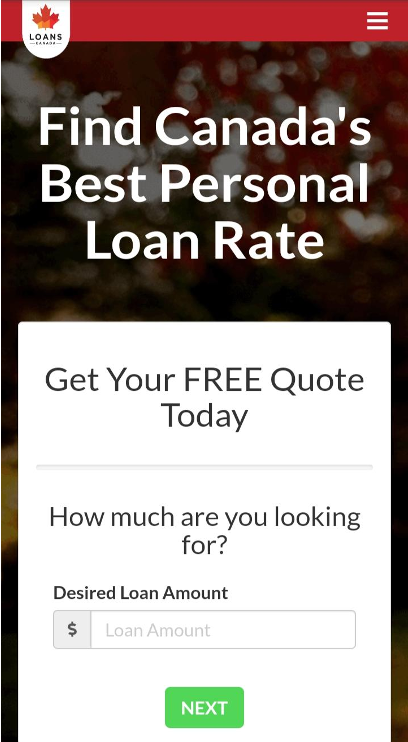

On the next page, you will be asked to input your desired loan amount. Your input must be in digits/numbers only. Click next after inserting your desired amount.

Here, you will have to indicate why you want to secure the loan e.g. card maintenance, credit card payoff, home improvement, utility bill etc. Click next after indicating the purpose of the loan.

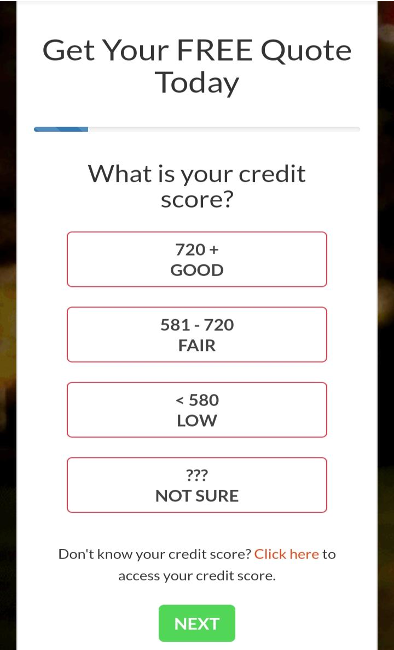

This page displays different ranges of credit score from which you must choose the range your credit score falls under. The ranges are rated as, “good,” “fair,” and “low.” Choose and click next.

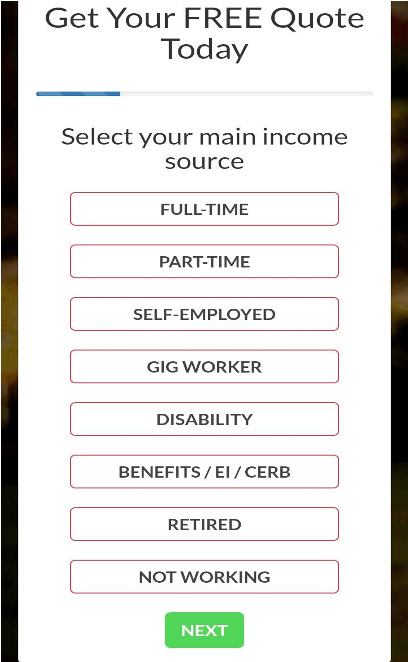

On this page, you will be asked to indicate your main source of income e.g Fully employed, self employed etc.

The following steps will require you to input more personal details such as postal code. Afterwards, you will be asked to submit your request.

Once you are matched with a lender, consider the terms and ensure that the repayment plan suits your budget before accepting.

Here, the loan funds are debited into your account.

Frequently asked questions

What happens after I am approved?

What if I have been denied previously?

I just immigrated to Canada; do I qualify?

Will my application affect my credit score?

Can I Apply If I am Self-Employed?

Is LoansCanada.ca service free?

Conclusion

While Loanscanada may have reduced the stress of finding the right lender for you, it is advisable to do your due diligence before signing on the line. Go through the reviews of the lenders recommended for you. Loanscanada services are undoubtedly beneficial to anyone seeking a quick loan, but it is wise to be aware of the extent of liability borne by Loanscanada as well as disclaimer. It is important to read through all the terms and conditions attached to the transaction before signing.

Piggyy

״The secret of happiness, is not found in seeking more, but in developing the capacity to enjoy less״ - Socrates

Share this article: